The Importance of the State Pension Age

The state pension age (SPA) in the UK is a crucial aspect of the welfare system that significantly impacts millions of citizens. It dictates when individuals can begin to receive their state pension—a vital source of income for many during retirement. As life expectancy continues to rise, discussions surrounding the SPA have become increasingly relevant, prompting considerations for adjustments to the eligibility criteria.

Current State Pension Age

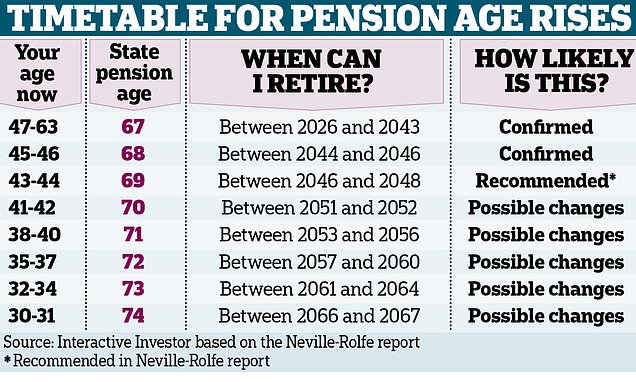

As of October 2023, the state pension age for both men and women in the UK is set at 66 years old. This age is scheduled to rise to 67 between 2026 and 2028 as part of a phased approach to ensure that the state pension system remains sustainable for future generations. The government plans to further review the SPA, with proposals to potentially increase it to 68 years by the mid-2030s. These reforms are driven by the need to adapt to demographic changes in the population.

Public Reactions and Concerns

Recent discussions in the media and parliamentary debates have ignited public interest and concern over the government’s plans for the state pension age. Many individuals nearing retirement express anxiety regarding these changes, particularly those who may have planned their financial futures based on the existing pension age. Additionally, there are apprehensions about the impact on health and employment for older workers.

Government’s Rationale

The rationale behind increasing the state pension age is informed by a combination of factors, including increased life expectancy and the need to relieve fiscal pressure on the nation’s finances. The government maintains that these measures are necessary to protect the integrity of the state pension system, ensuring it remains viable for future retirees.

Future Expectations

Looking ahead, anticipated reviews by the government regarding the state pension may bring about further changes. With an ageing population and increasing longevity, experts predict that the government will need to continue adjusting the SPA to reflect these demographic shifts continually. Stakeholders in pension planning—including employers, financial advisors, and the public—will need to remain vigilant as these discussions evolve.

Conclusion

The state pension age in the UK is more than just a number; it is a complex issue of social and economic importance. With reforms on the horizon, understanding the implications of the state pension age will be crucial for current and future retirees alike. As the situation develops, it will be vital for individuals to keep informed and adjust their retirement plans accordingly.

You may also like