Introduction

The Bank of England base rate plays a pivotal role in shaping the economic landscape of the United Kingdom. As the key interest rate set by the central bank, it influences borrowing costs for consumers and businesses alike. Recent fluctuations in this rate have garnered significant attention, given their implications for inflation, mortgage rates, and overall economic growth.

Recent Developments

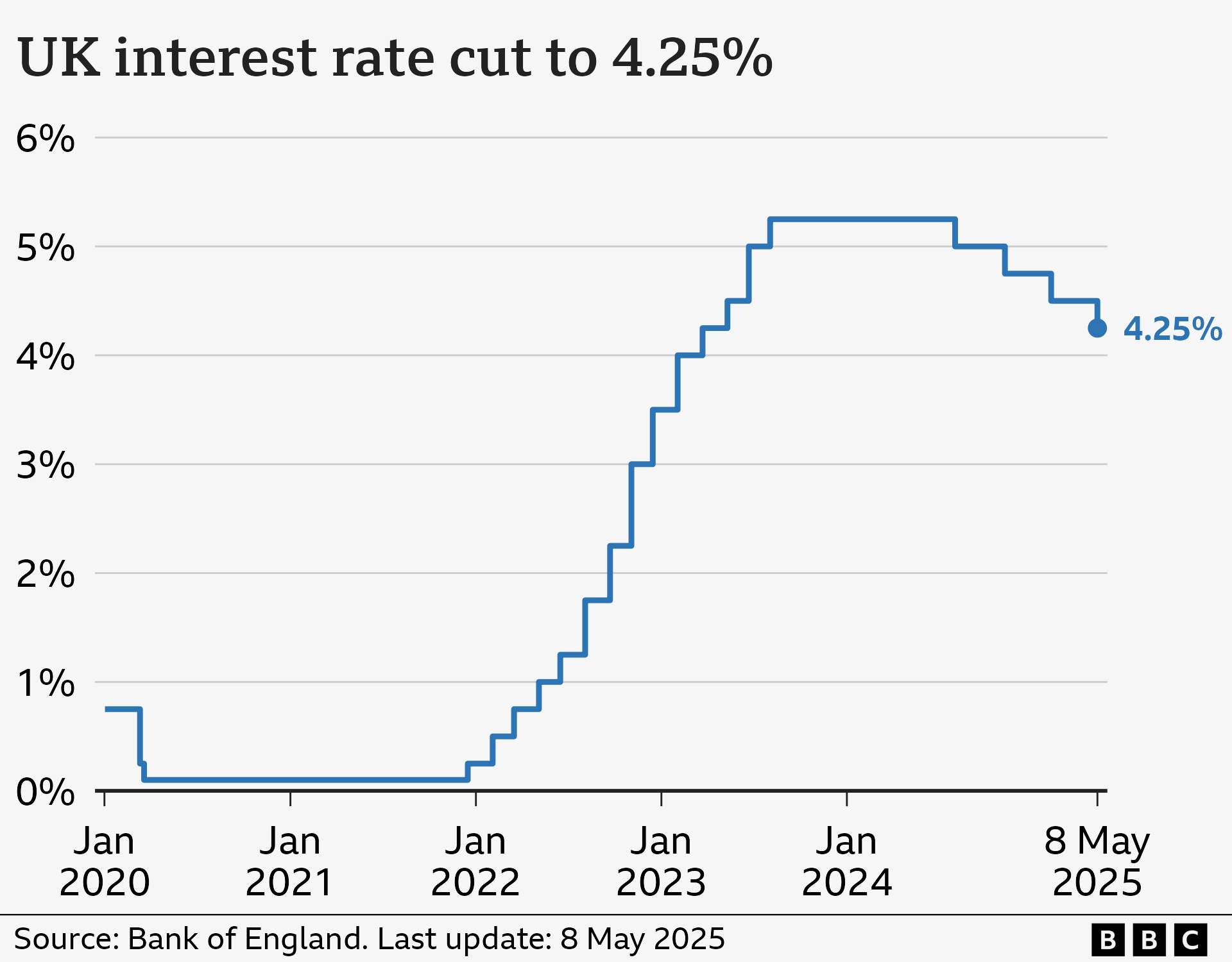

As of November 2023, the Bank of England has maintained its base rate at 5.25% following a period of intense monetary policy adjustments aimed at addressing persistent inflationary pressures. The decision reflects the central bank’s commitment to ensuring price stability in the face of ongoing economic uncertainties, including geopolitical tensions and the effects of the COVID-19 pandemic recovery.

The latest meeting of the Monetary Policy Committee (MPC) highlighted concerns over inflation, which remains above the government’s target of 2%. According to the Office for National Statistics, the Consumer Prices Index (CPI) inflation rate was recorded at 4.8% in October, a slight decrease from September’s figure. However, the committee indicated that further adjustments to the base rate may be necessary if inflation does not continue to decline.

Impact on Borrowers and Savers

For borrowers, the current base rate means that mortgage repayments remain relatively high, particularly for those with variable-rate mortgages. Homeowners have expressed concerns about affordability as continued rate stability is crucial for planning finances. Conversely, savers may benefit from higher interest rates on savings accounts; however, the low return relative to inflation has prompted calls for banks to offer more competitive rates.

Future Outlook

Analysts predict that the Bank of England might consider further adjustments to the base rate in the coming months, contingent on inflation trends and economic growth patterns. The GDP data indicates a slow but steady recovery, raising the question of whether the central bank will adopt a more aggressive stance in future meetings.

As the cost of living crisis continues to affect households across the UK, the Bank of England faces the challenging task of balancing rate changes that support economic growth while controlling inflation. Stakeholders from all sectors will be watching closely to see how these decisions unfold.

Conclusion

The Bank of England base rate remains a crucial tool in managing the UK economy, influencing various financial aspects from borrowing to savings. Understanding its current position and potential future movements is essential for both consumers and businesses as they navigate the evolving economic climate. Maintaining awareness of monetary policy changes will help individuals and companies make informed financial decisions in these unpredictable times.

You may also like