Introduction

Pensions inheritance tax is an increasingly important consideration for individuals in the UK as they plan their estates. With many people relying on pensions for retirement, understanding the implications of inheritance tax (IHT) on these financial assets is crucial. The changing landscape of tax legislation and pension rules makes it essential for individuals to be informed about how pensions can affect their beneficiaries’ tax liabilities.

What is Pensions Inheritance Tax?

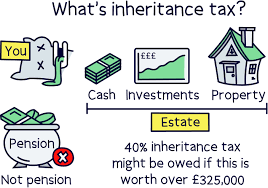

Pensions inheritance tax refers to the tax levied on the value of a pension pot that is passed on to beneficiaries upon the death of the account holder. In the UK, pensions are generally exempt from IHT; however, the specifics can vary depending on the type of pension scheme and the age of the policyholder at the time of death.

Tax Implications Based on Age

If an individual dies before the age of 75, their pension can typically be passed on to beneficiaries tax-free, allowing them to withdraw the remaining pension funds as lump sums, annuities, or drawdowns without incurring any tax. However, if the individual dies after reaching the age of 75, pensions are subject to income tax when beneficiaries withdraw funds. This means they could face a tax bill based on their income tax rates, which may significantly impact the value of the inheritance.

Recent Changes in Legislation

Recent reforms have sought to simplify the process and reduce the tax burden on individuals passing on their pensions. For instance, changes implemented during the last few years have ensured that more individuals can take advantage of tax-free withdrawals, and there have been discussions about further reforms to alleviate potential tax liabilities on pension funds.

Planning Strategies to Mitigate Tax

For those concerned about pensions inheritance tax, several strategies can help mitigate potential liabilities. One common approach is to ensure that the pension holder maintains an up-to-date expression of wish form, indicating who they would like the funds to go to after their death. Additionally, individuals can consider taking out life insurance policies to cover potential tax liabilities, ensuring that beneficiaries receive the full value of the pension.

Conclusion

As the laws governing pensions inheritance tax continue to evolve, understanding the potential implications for your estate planning is imperative. While pensions can often provide a tax-efficient method of passing wealth onto the next generation, it is wise to consult a financial adviser or tax professional to navigate the complexities involved effectively. Planning ahead can provide peace of mind and ensure that your intended beneficiaries receive maximum benefit from your financial legacy.

You may also like