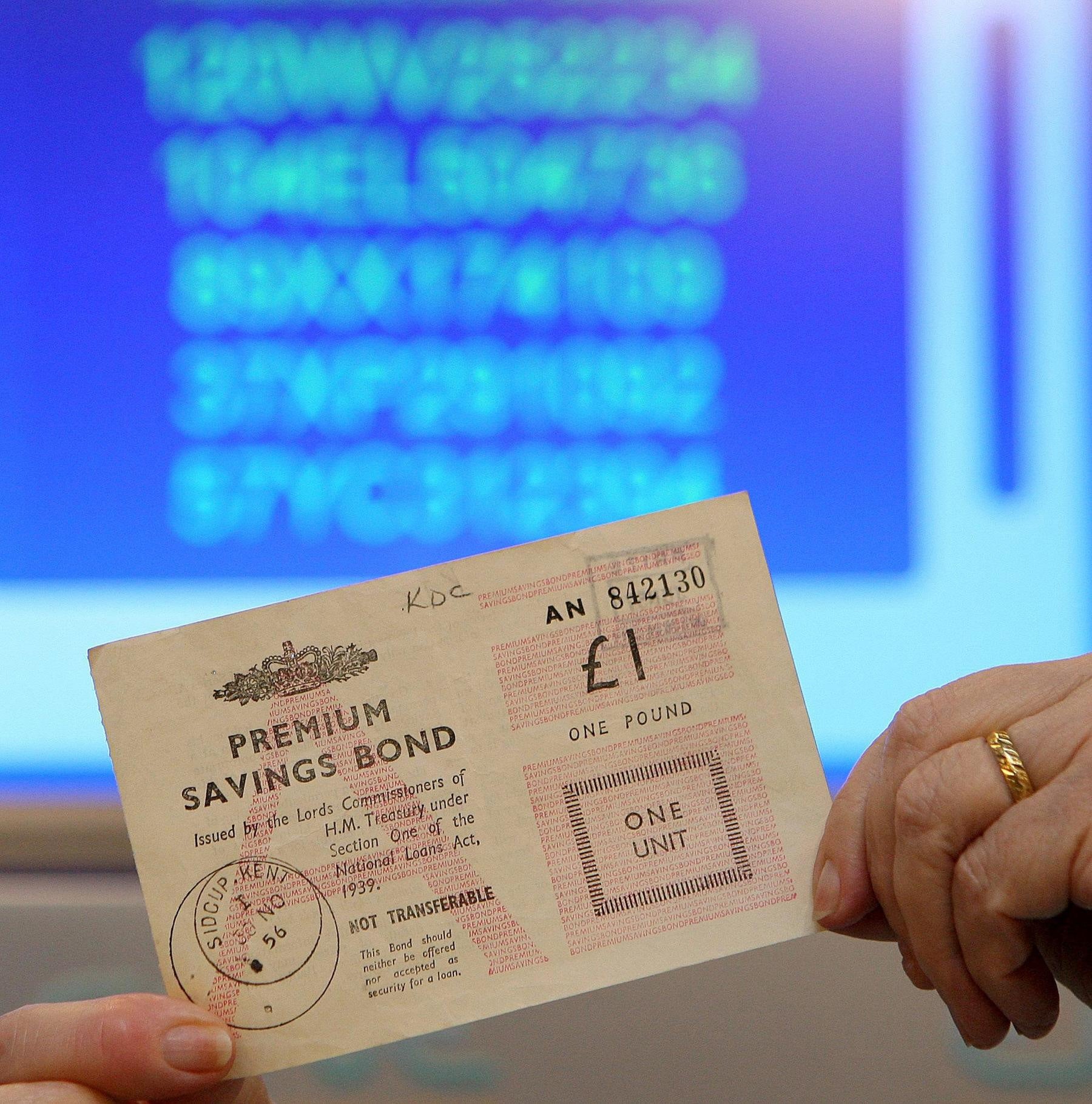

Introduction to Premium Bonds

Premium bonds, introduced in the UK in 1956 by National Savings and Investments (NS&I), remain a popular choice for savers seeking a unique alternative to traditional savings accounts. With the current economic uncertainty and fluctuating interest rates, understanding premium bonds has become increasingly relevant for individuals looking to maximise their savings while enjoying the possibility of tax-free winnings.

The Current Interest in Premium Bonds

As of 2023, the total number of active premium bond holders has surpassed 23 million, holding more than £100 billion in bonds. Premium bonds offer no guaranteed return; instead, holders have the chance to win tax-free cash prizes ranging from £25 to £1 million in monthly prize draws. This gamble on luck appeals to many, particularly in a climate where interest rates on savings accounts are often lower than inflation, effectively eroding savings over time.

Recent Changes and Prize Draws

Recent reforms have seen NS&I increase the prize fund rate to 3.00% from 1.40%, enhancing the attractiveness of premium bonds. Each £1 bond qualifies for a chance to win in the monthly draws, with the first draw of the year in January 2023 revealing 5.4 million prizes totaling £242 million. Such improvements signify NS&I’s commitment to ensuring premium bonds remain competitive amidst changing financial landscapes.

Advantages and Challenges

The key advantage of premium bonds is their flexibility; investors can cash in their bonds at any point without incurring any penalties, making them a highly liquid investment. Additionally, since winnings are tax-free, this is particularly appealing for higher-rate taxpayers. However, the lack of guaranteed returns makes them less appealing for those seeking steady income from their savings.

Who Should Consider Premium Bonds?

Premium bonds can be a suitable option for individuals looking for a saving solution that balances the security of their capital with the excitement of potential prizes. They are particularly attractive for those who might not require immediate access to the funds but are also willing to take the risk of not winning anything at all.

Conclusion: The Future of Premium Bonds

Looking ahead, premium bonds will likely continue to be a staple for UK savers, especially within an unpredictable economic environment. As savings products evolve, NS&I’s adjustments reflect an adaptable approach to consumer needs, ensuring that premium bonds maintain their relevance in personal savings strategies. Whether viewed as a novelty or a strategic investment, investors should consider their individual financial goals when deciding on premium bonds.

You may also like