Introduction

The phenomenon of a house prices crash has significant implications for homeowners, investors, and the broader economy. As the UK navigates a turbulent economic landscape, recent reports indicate a notable decline in house prices across various regions. This downturn raises questions about the future of the housing market and the consequences for both current homeowners and prospective buyers.

Current Trends in House Prices

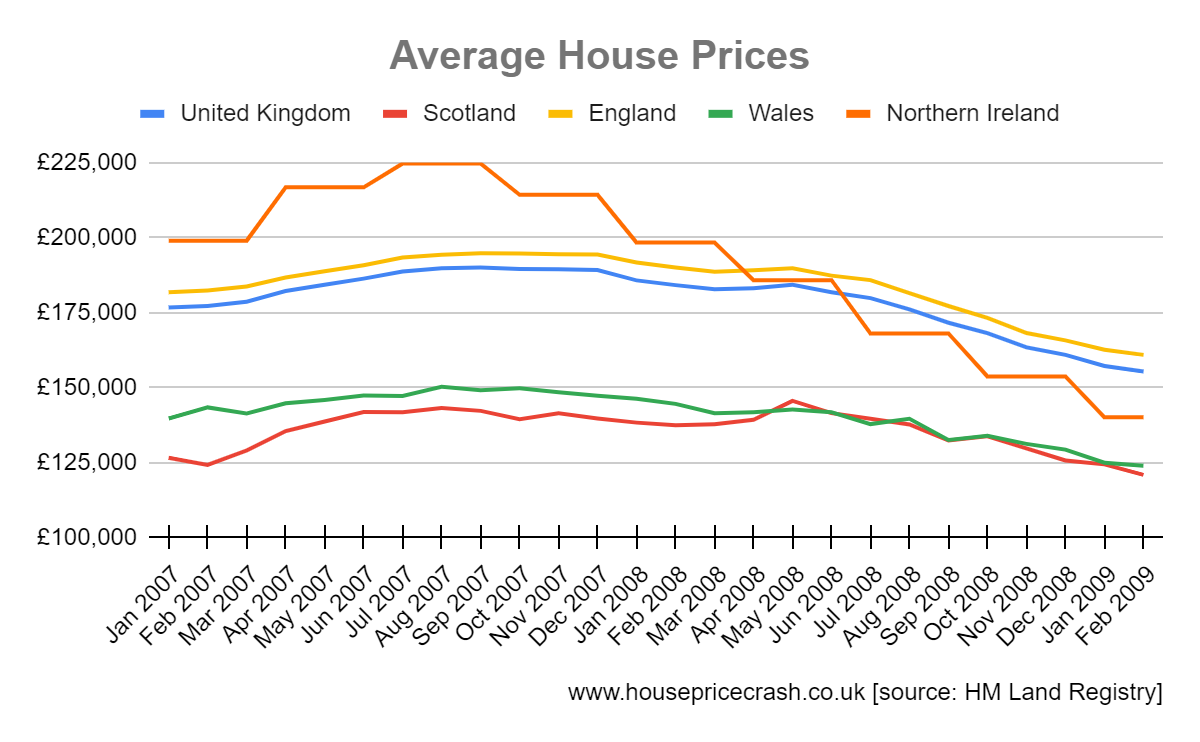

According to the latest figures from Nationwide Building Society, UK house prices fell by 5.3% in September 2023 compared to the same month the previous year, marking the most significant annual drop since 2009. Factors contributing to this decline include increased interest rates, which have made mortgages more expensive, and rising living costs that have squeezed household budgets.

The Bank of England’s monetary policy, aimed at curbing inflation, has led to a series of interest rate hikes that have significantly impacted borrowing costs. With the base rate reaching 5.25%, many potential homebuyers are finding it increasingly difficult to secure affordable financing, thus reducing demand in the housing market.

Regional Variations

The impact of the house prices crash is not uniform across the country. Regions such as London and the South East have seen more pronounced declines, with some areas experiencing drops of up to 10%. In contrast, regions in the North, while still facing declines, are less affected, although they are not immune to the overall trend.

Implications for Homeowners and Buyers

For existing homeowners, the decline in property values may lead to negative equity situations, where individuals owe more on their mortgages than their properties are worth. This scenario can limit homeowners’ ability to move or refinance and could lead to increased financial distress. On the other hand, potential buyers may see this as an opportunity to enter the market, but they must also consider the higher costs associated with mortgages.

Looking Ahead

Economists suggest that the housing market may continue to face pressure as inflation remains a concern, and interest rates could remain elevated. There is a possibility that the trend of declining house prices could continue into 2024, depending on economic recovery and the government’s fiscal policies. For potential buyers, waiting for the market to stabilise may be a prudent choice, albeit with its own risks.

Conclusion

The crash in house prices has far-reaching implications for the UK housing market, reflecting economic challenges and shifting consumer behaviour. Homeowners and buyers alike must navigate a changing landscape marked by uncertainty. As we move into the coming months, all eyes will be on indicators of economic recovery and the potential for a stabilising housing market.

You may also like