Introduction

The government state pension age is a crucial topic for millions of UK residents as it impacts financial planning and retirement. Recent discussions about potential changes to this age have brought the subject to the forefront of public interest, especially with the challenges posed by an aging population and economic pressures. Understanding these changes is vital for those nearing retirement and their families, as it affects not just their income but also their work-life balance and retirement planning.

Current State Pension Age

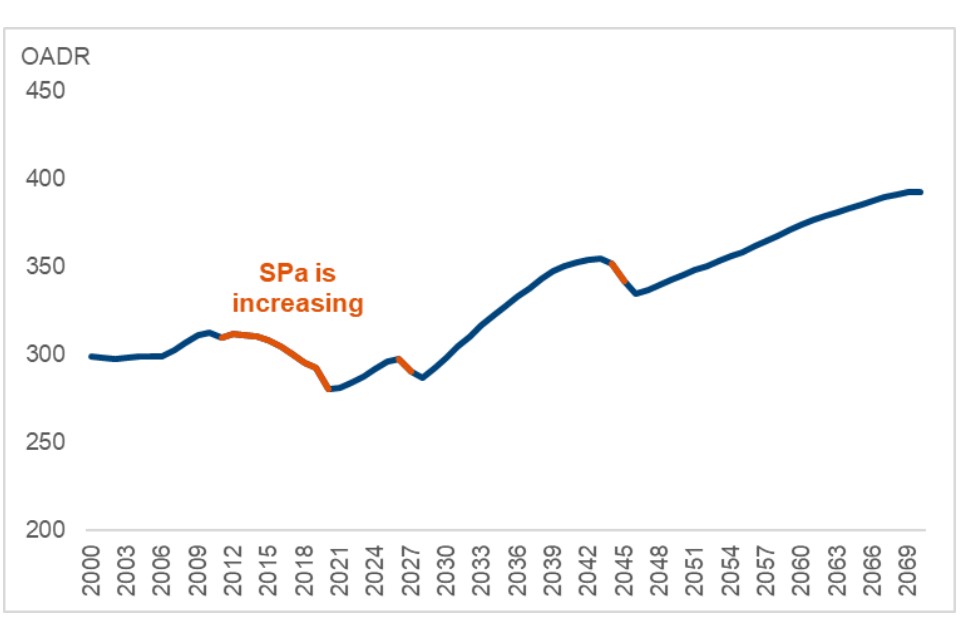

As it stands, the state pension age for both men and women in the UK is set to rise to 67 years by 2028. This change was enacted as part of the government’s efforts to ensure the sustainability of the pension system in light of increasing life expectancy. According to the Office for National Statistics, life expectancy has risen significantly over the past few decades, requiring adjustments to the pension framework to accommodate longer lives and changing demographic trends.

Proposed Changes and Public Reaction

Recently, discussions have surfaced regarding the possibility of increasing the state pension age to 68 by as early as 2039 or even earlier, in a bid to cope with financial challenges posed by rising costs and longevity. These proposals have sparked a mixed response from the public and various stakeholders. Some argue that raising the age further is necessary for financial stability and to ensure continued support for the next generations. Others express concern that such changes could disproportionately affect those in physically demanding jobs, who may find it difficult to work longer.

Implications for Future Retirees

The implications of any changes to the government state pension age could be profound for future retirees. Those planning their retirement will need to recalibrate their savings and investment strategies to account for a potential delay in pension payouts. Additionally, many people may need to adjust their expectations regarding retirement age and lifestyle. Financial advisors are urging individuals to start planning early and consider alternative income sources in the event of changes.

Conclusion

In conclusion, while the state pension age has been a longstanding topic of discussion, the recent proposals call for an immediate reassessment by individuals nearing retirement. It remains essential for the government to balance fiscal responsibility with fairness for the workforce. Looking ahead, it will be crucial for policymakers to engage with the public, providing clear communication and support to navigate the complexities surrounding the state pension age. As the situation develops, those affected should stay informed and proactive about their retirement planning.

You may also like